Cola Wars Continue: Coke and Pepsi in 2010 Case Study Solution

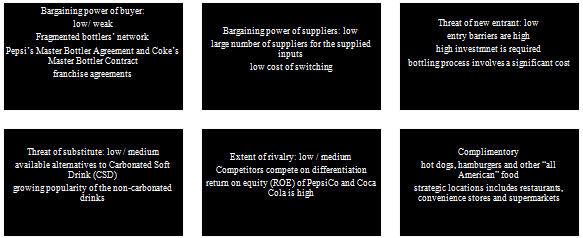

Extent of rivalry

There are two leading and valuable brands in the market that have claimed the market share of 72 percent of sales volume of CSD by 2009, hence followed by Dr Pepper Snapple Group (DPS),which in year 2009, anticipated to hold the Cott Corporation (4.9 percent) and 16.4 percent market share.

It is also analyzed that the competitors do not compete on pricing, but on differentiation, hence keeping the industry growing and profitable. Also, the return on equity (ROE) of PepsiCo and Coca Cola are 35.4 percent and 27.5 percent by 2009,respectively. These brands put their major emphasizes on non-price factors such as lifestyle advertising and product innovation rather than on price of product. Even if the brands have faced the price wars during 70s and 80s, they now prefer to differentiate themselves to prevent the falls in profit returns.

Complementors

It is imperative to note that there are various complementors that can positively impact the demand for Pepsi & Coke, such as hot dogs, hamburgers and other “all American” food. There is a high influence of complementors due to the fact that the complements can be the choice of strategic locations, which increase the profitability. The soft drinks are available in restaurants, convenience stores and supermarkets.All of such places tend to make these products handy to the customers.

Strategy Formulation and Its Implications

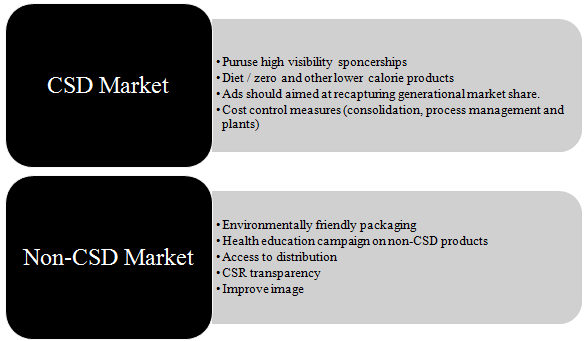

The two valuable and renowned brands Pepsi and Coke can sustain and bolster their profit margin in the wake of growing popularity,by reducing the demands of non-CSDs via various strategic actions. Since, the preferences of the customers are changing constantly, it is important for the brands to proactively monitor the factors in external environment in order to obtain the valuable information in response to the production planning. The brands need to come with the new non-CSD product line or they need to acquire the established non-CSD brands,who already have an efficient production and operation.

The brands should conduct surveys so that they could gain the consumers’ insights on forms of non-CSD beverages that they wish or like to have.Another recommended action is that the brands should consider the leverage knowledge of marketing competency, customer base and established channel of distribution through diversifying into healthy snack items after analyzing the attractiveness of the market (Lee, 2009). They should innovate or ignite the bottled water, engage in green activities and offer convenient and healthy choices for people with busy lifestyles. Not only this, the brands should also pursue the high visibility sponsorship. They should explore the product development and market research innovation opportunities. The companies can go for vertical integration, and buy the suppliers of their inputs or they could venture into distribution or buy the final producers of their product. Such integration would allow them to bolster profits and grow as well as flourish in such competitive market. The brands should also bring innovation in value chain such as distribution, manufacturing,packaging and other value chain steps(Birkinshaw, 2007).

Conclusion

To sum up, it is to conclude that the two valuable brands Pepsi and Coke have controlled and have been dominating the carbonated soft drinks industry for decades, but now these brands are experiencing the continuous and significant drop in sales due to the changes in their external environment.The critical issues include decline in CSD sales, which further includes Cola in the United States.It is due to the fact that the price sensitive consumers have cheaper alternative easily available to them, such as tap water of private label bottles water that tend to exhibits the little loyalty of these consumers towards the brands in comparison to CSD. Another reason of decline is the health issues such as nutrition and obesity.The bottlers’ network is fragmented, while having limited power of negotiation with the concentrated producers.Pepsi has purchased two of its biggest bottlers, also, the largest bottler of Coke known as Coca-Cola Enterprise (CCE), which handles 75 percent of Coke’s North American Bottle and logged sales on annual basis for more than 21 billion dollar has been purchased by Coke in 2010. Thus, the market contains various suppliers for the supplied inputs & the low switching cost on the basis of the needs and cost, limiting the bargaining power of supplier.The competitors do not compete on pricing, but on differentiation, hence keeping the industry growing, flourishing and profitable.

Exhibit A – Six Forces

Exhibit B – Action Plan

This is just a sample partical work. Please place the order on the website to get your own originally done case solution.

Related Case Solutions & Analyses:

Marketing Analysis Toolkit: Breakeven Analysis

Marketing Analysis Toolkit: Breakeven Analysis

Recent Developments in the Ranbaxy Case

Recent Developments in the Ranbaxy Case

Merchant Card Services Inc. (A)

Merchant Card Services Inc. (A)

ConAgra Foods

ConAgra Foods

MontGras: Export Strategy for a Chilean Winery

MontGras: Export Strategy for a Chilean Winery

International Alliance Negotiations: Legal Issues for General Managers

International Alliance Negotiations: Legal Issues for General Managers

Dreyers Grand Ice Cream (C)

Dreyers Grand Ice Cream (C)

Collapse in Asia–1997-98

Collapse in Asia–1997-98

Paint-Pen Inc.

Paint-Pen Inc.

DigitalThink: Building a Sales Force

DigitalThink: Building a Sales Force